Part 6 of ‘Climate Policies and Instruments’ series

Steam released on the streets of New York (Source: Gary Hershorn/Getty Images)

Blogs 18, 19, and 20, introduced Social Cost of Carbon (SCC), discussed the two popular approaches for thinking about and framing the Social Cost of Carbon (SCC)—a marginal damages-based approach and a marginal abatement cost-based (MAC) approach, and explored the challenges and uncertainties in the evaluation process. This blog extends this discussion further to present the role and significance of Social Discount Rate.

Let’s start with something simple. If we have two choices, “work today and get paid today” vs. “work today and get paid after a year”, we are mostly likely to pick the first option. The value of money decreases over time.

Now consider a different scenario. We have two choices again, “work today and get paid $100 today” vs. “work today and get paid $1000 after a year”. Now this is a tempting offer, yet patience matters. It’s possible some of us would prefer taking the $100 today than waiting for a ten-fold increase after a year.

One last scenario. Two choices; “work today and get paid $100 today” vs. “work today and get paid $100,000 after 10 years”. More than patience, here one needs perspective and willingness to think about the future which is filled with uncertainties.

The Social Discount Rate for SCC has similar variables and dilemmas in play.

Higher vs. Lower Social Discount Rate

‘Economic discounting’ refers to converting a policy’s future value to an equivalent present value, by applying a ‘discount rate’ for reduction. A higher discount rate suggests greater importance for present benefits, while a lower discount rate prioritises future benefits. Discount rates in Cost-Benefit Analyses (CBAs) or any policy or project appraisal operate under the assumption that people value immediate benefits highly over long-term gains. This is unarguably the most controversial topic of discussion in the context of SCC, as GHGs have long residence periods in the atmosphere, and the benefits of climate policies are expected to be delivered over centuries, unlike other conventional infrastructure development programmes.

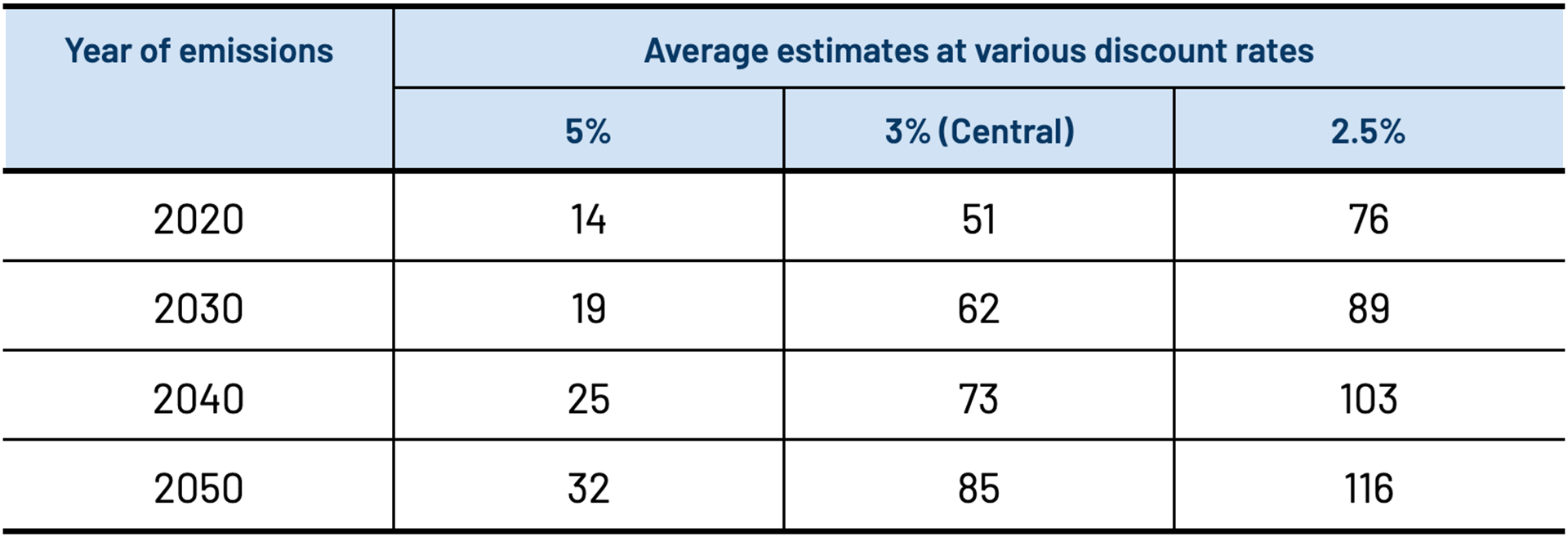

The Interagency Working Group (IWG), convened by the Obama administration in 2009 to estimate the SCC, proposed discount rates of 2.5, 3, and 5 percent and a central value of $45 per metric tonne of CO₂ (in 2020 dollars). In 2017, Trump’s office dissolved the IWG, and the federal agencies adopted 3 and 7 percent discount rates and a SCC as low as $1 per metric tonne of CO₂ (in 2020 dollars), without accounting for global impacts. In 2021, Biden’s office reinstated Obama’s values for the SCC, correcting it for inflation, and announced an interim central value of $51 per metric tonne of CO₂ (in 2020 dollars). In 2022, the Environment Protection Agency (EPA) revised the numbers with discount rates of 1.5, 2, and 2.5 percent and proposed a central value of $190 per metric tonne of CO₂ (in 2020 dollars), nearly a four-fold increase from Obama’s proposal. This shows the influence of discounting in estimating the SCC and the recent acceptance of using lower discount rates.

Table showing the influence of discount rate in estimating the SCC (2020$ per ton of CO₂), Source: Federal interim social cost of CO₂ estimates provided by the IWG under Executive Order 13990

Discount Rate and the NY Climate Act

The NY Climate Act directs “.....utilizing a range of appropriate discount rates, including a rate of zero.” This suggestion for a ‘zero discount rate’ goes beyond the conventional practice of referring to market return rates, for fixing SCC discount rates, and places equal weightage on the benefits for present and future generations. However, ‘Establishing a Value of Carbon: Guidelines for Use by State Agencies’ (EVC Guidelines) don’t prescribe a ‘zero discount rate’, instead recommend that the state agencies use a range of discount rates, between 1 and 3 percent, for a thorough analysis and present their assessment with 2 percent as the central value for decision-making. This abides by the EPA’s proposed SCC values, covers global impacts, and addresses intergenerational equity concerns. This could also be viewed as a progressive position, compared to the commonly used 2.5 percent or higher discount rate by other states, including Washington.

But has this resolved the ‘discounting controversy’ forever? - NO.

While there is broader agreement on using ‘lower discount rates’ for climate policies, ‘how low’ is still an area of debate. Experts cite varied reasons for adopting a ‘zero discount rate’, including uncertainties in future wealth accumulation and distribution, the inapplicability and inappropriateness of economic valuation in deciding basic human rights-related actions, and the potential existential impacts of climate change. Conversely, a camp of economists also warns that evaluating benefits expected after centuries, similar to present gains, could increase the SCC exponentially and demand substantial sacrifices from the present generation. Hence, NY could adopt two thumb rules: 1) incrementally reduce discount rates, after annual reviews of economic growth, and 2) adopt lower discount rates (or zero discount rate) for climate policies with long-horizon periods and targeted at vulnerable communities.

This will allow the NY state to follow Ramsey’s approach, capturing the “rate of pure time preference” in valuing the welfare of future generations, and include an adjustment mechanism that compensates for the changes in dollar value. In simple terms, a framework that links the discounting rate and economic growth could be created (NASEM). For instance, the estimates from the Resources for the Future (RFF) recommend 1.7 as the effective near-term discount rate for the NYS (not two percent or zero percent).

Such a flexible and continuously evolving discounting framework and practice would also align with the long-term transition to the MAC approach, as regular revisions to MAC curves, discounting rates, and accordingly to the ‘value of carbon’ could become a periodical institutional commitment (every three to five years) with dedicated resources.

SCC and the Clean Energy Economy Goal

The ‘clean energy economy’ goal of the NY Climate Act covers both territorial and consumption emissions with special attention being guaranteed for the just socio-economic transitions of the most vulnerable communities. Placing an accurate and updated ‘value of carbon’ (SCC) is key to fulfilling this through the most cost-effective climate policies. Hence, the numerous uncertainties in the valuation and application of SCC can never be the reason for its complete dismissal. NY’s focus should be on consistent improvement.

Though improving the precision of the SCC largely depends on overall global scientific research and technological advancements, 'political commitment' and fair institutional 'value judgement' also play a significant part in embedding ‘intergenerational equity’ and ‘social justice’ in appraising policies and projects. Therefore, the NY’s Climate Action Council, working in collaboration with the environmental justice advisory group and the climate justice working group, has the responsibility of keeping up the ‘integrity’ of SCC valuation and application.

Let’s remember, achieving net zero does not promise ‘zero climate damages’. The long-horizon period of GHG emissions will likely have a longer, disastrous impact, even after we adopt low discount rates and stop emissions. So, as we improve our metrics and modelling, we also need to enhance preparedness for future risks from the lens of vulnerabilities and social equity. SCC is one of the solutions that could take us closer to a resilient and inclusive future; not all.

Have questions, thoughts, or feedback? Write to nagendran.bala.m@gmail.com.