Part 3 of ‘Climate Policies and Instruments’ series

Aerial view of a factory emitting smoke (Source: The International Energy Agency)

In Blog 17, we looked at the need for and significance of combining economic instruments, like Carbon Tax, with Command-and-Control (CAC) policies to reduce emissions at the lowest cost, through the case of Germany’s Building Energy Act, 2023. Towards taking such a climate policy direction, it is critical to assign or know the cost of carbon emissions. In this context, this and the next three blogs will refer to the New York State Climate Act, 2019, to introduce the Social Cost of Carbon as a concept, discuss three key areas of technical controversy in estimating the value of carbon, and present some high-level recommendations for their adoption.

How much would the impact of climate change cost New York? How much should New Yorkers be willing to pay to protect them? How much do New Yorkers value the well-being of future generations over their present benefits? - The New York State’s (NY) ‘value of carbon’ estimate, presented as the social cost of carbon (SCC), attempts to answer these questions by putting a ‘present value’ to the future impact of greenhouse gas (GHG) emissions. Putting a price tag on a product is often the most complex activity, especially in the modern world, where engineered solutions and product value chains are more globally connected (and dependent) than ever before. And the task at hand is putting a price on a by-product (carbon emissions), keeping in mind its future impact—an even bigger challenge. The SCC frames this challenge, though not completely solved yet. Maybe, as Sammy Roth from the Los Angeles Times said, “There’s no such thing as a perfect climate change solution.”

The SCC, commonly estimated and represented in dollars (USD), converts the impact of climate change into economic terms. This is done by assigning a price to one metric tonne increase in carbon dioxide (CO₂) emissions (or other GHGs) in the atmosphere, in today’s socio-economic context, accounting for its projected future benefits or damages. This estimate is expected to steadily increase (annually), as present-day CO₂ emissions would have consequences for centuries and the stress on global physical and economic systems would compound with the climate crisis. Conceptually, a higher SCC not only signifies rising GHG emissions and the associated increase in future climate-related damages, but also the increased value the present society is willing to place on the safety of future societies.

Since 2008, when the Centre for Biological Diversity sued the United States (US) federal government over new fuel economy standards, accounting for climate impact has become a mandate in evaluating the benefits and costs of the country’s policies. The agencies meet this requirement by multiplying a prescribed or identified ‘SCC value’ with the projected increase or decrease in tonnages of emissions, due to a proposed policy or project. Hence, SCC, as an ‘economic measure of climate mitigation’, supports decision-making through its application in cost-benefit analyses (CBA), impact assessments, carbon taxation, climate subsidy frameworks, and emissions target planning.

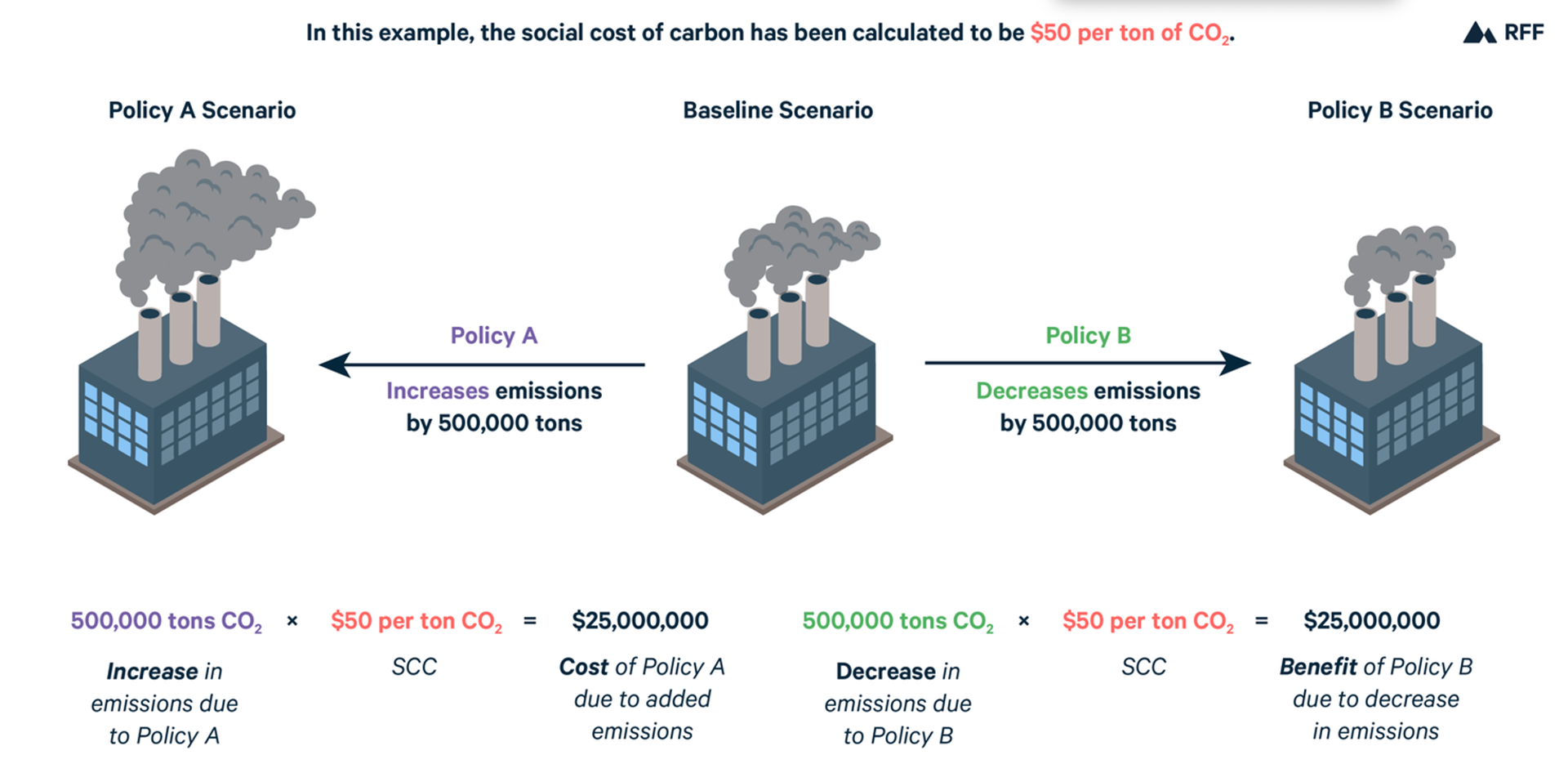

Illustration depicting the application of SCC in CBAs (Source: RFF)

Recognising the role of this “most important number,” NY’s Climate Leadership and Community Protection Act, 2019 (CLCPA), through the article ‘75-0113: Value of Carbon,’ directed the Department of Environmental Conservation (DEC) to “....establish a social cost of carbon expressed in terms of dollars per tonne of carbon dioxide equivalent ($/tonne CO₂e),” within a year, for use by state agencies. In response to this directive and to achieve the statutory 2050 net-zero target, the first guidance was released in 2020. ‘Establishing a Value of Carbon: Guidelines for Use by State Agencies’ (EVC Guidelines), published in August 2023, is the most recent update for conducting project-level CBAs.

The next three blogs pick this publication to discuss in detail three components that shape the SCC; 1) the approach to valuation - damages-based vs. abatement-based; 2) the process of economic modelling and working with uncertainties; and 3) the discount rate parameter that determines integrity and equity for application.

Read Blog 19: Social Cost of Carbon: Approach to Evaluation

Have questions, thoughts, or feedback? Write to nagendran.bala.m@gmail.com.